Peer-to-Peer Lending is Better Than Bonds

- Even over longer periods of time, bonds have barely kept up with rising prices – and perhaps not even that.

- Peer-to-peer lending has easily given investors solid real returns over all time periods.

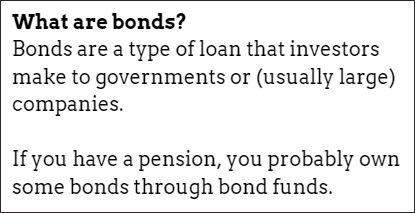

How good are bonds?

On average, bonds are “a bit naff”, according to the fantastic Credit Suisse Global Investment Returns Yearbooks.

OK, the Credit Suisse funded research doesn't actually use those words, but it does show it through its figures and graphs.

The research shows that, in 113 years, shares would have made you over 300 times richer. For corporate bonds, on the other hand, the real rewards haven't even increased wealth by eight times. Far less than that if you include government bonds.

Worse, the Credit Suisse research doesn't consider investing costs. It's not free to buy and sell bonds, because there's some middleman charging you somewhere.

Even worse, when most of us invest in bonds, we do so through bond funds, so that those of us who aren't rich can more easily spread our risks across more bonds. Funds add an extra layer of annual management charges and expense costs, which further reduces average returns.

After costs, the result is that you're not really likely to do much better than savings accounts and you're going to struggle to protect your wealth from rising prices.

Where exactly is the pay-off for bonds?

Astoundingly, you're not even getting great stability in return for these lower rewards. You can invest in bonds on a monthly basis for well over 30 years and still be poorer in real terms at the end. That is not a one-off incident localised in one country, but an event that has happened many times in many places.

And over the short- or even medium-term, you can make some quite significant losses.

It seems to me that the rewards are more volatile than you deserve, considering the meagre potential returns.

Can you be an above average bond investor?

I try to see the positives of bonds, I really do. For example, we're just talking averages here, so some people must do a whole lot better. But, with such a record, it's hard to imagine why anyone would invest in lots of bonds regularly.

I think it makes more sense to save and invest where the odds are already stacked in your favour.

I also like to bear in mind that the excellent researchers who write the Credit Suisse report* have the view that bonds smooth out returns for stock-market investors. But this smoothing comes at a very high price.

And what about peer-to-peer lending?

Many years ago, nearly ten years after peer-to-peer lending started, I first wrote on this very page – now updated – that the vast majority of UK lenders have easily made money.

It's now nearly 20 years since P2P began, and the situation across all of Europe is the same: the industry has seen at least two recessions in most countries during this time. Many countries have also suffered property market crashes. Yet lenders have easily made money over both the short and long term.

I wrote back then that 10 years is not very long and the future is always different to the past. Today, I say that 20 years is also not extremely long compared to other types of investments. But the risk-reward profile of lending to consumers, businesses and against property is well-known. Conservative, low-risk lending practices result in relatively few bumps and yet decent returns.

Why take the risk?

You could go for low-risk bonds and hope that you'll manage to get a real positive return, or even a neutral return (so much for “low risk”). But surely it's better to go for something that's likely to give a real positive return – especially when you take simple steps to manage the risks further to greatly increase your odds?

Further reading

Read Peer-to-Peer Lending vs Bonds | Why Does P2P Lending Pay Investors Higher Rates Than Bonds? | Peer-to-Peer Lending Vs Other Investments.

Pages linked to above:

Independent opinion: 4thWay will help you to identify your options and narrow down your choices, but the decision is yours. We're responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or any of the domestic financial regulators in Europe. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

*Credit Suisse Global Investment Returns Yearbooks are written by the London Business School professors Elroy Dimson, Mike Staunton and Paul Marsh. These professors also wrote the investment classic: “Triumph of the Optimists: 101 Years of Global Investment Returns”.

This page was adapted from our UK website. The original is here.